In a major fire that broke out in a cargo ship carrying nearly 3,000 cars off the Netherlands coast, an Indian crew member was killed and 20 others were injured. Dutch coastguards warned that the fire could last days.

As maritime commerce evolved and the global economy became increasingly interconnected, the need for safeguarding valuable cargo, vessels, and businesses against uncertainties became apparent. Enter marine insurance – a financial lifeline for those venturing into the cargo business, ensuring their investments are shielded from the tempestuous elements and unforeseen perils. In this article, we embark on a journey to explore the delicate domain of marine insurance. We will try to unravel its features and characteristics that have weathered the test of time. We will dive into the depths of marine insurance to illuminate its vital role in safeguarding a maritime world in constant motion. Join us as we uncover the essence of marine insurance.

What is Marine Insurance?

Loss or damage to cargo or goods occurring during transportation from the point of origin to the point of destination is covered by a marine policy. According to Section 5 of the Marine Insurance Act of 1906 (MIA), anyone with an insurable interest may purchase a marine insurance policy. Marine insurance policies come in a variety of forms, including those for courier and postal services, as well as for land, air, rail, and sea transportation.

The most frequent reasons for marine cargo loss during transit include fire, explosion, hijackings, accidents, collisions, and overturns. A marine insurance policy might provide carefully crafted plans, in addition to covering theft, malicious damage, shortages, non-delivery of products, damages during loading and unloading, and cargo mishandling. Depending on business requirements, coverage can be tailored, and it is offered for a wide range of cargo and items, whether you are a manufacturer or trader.

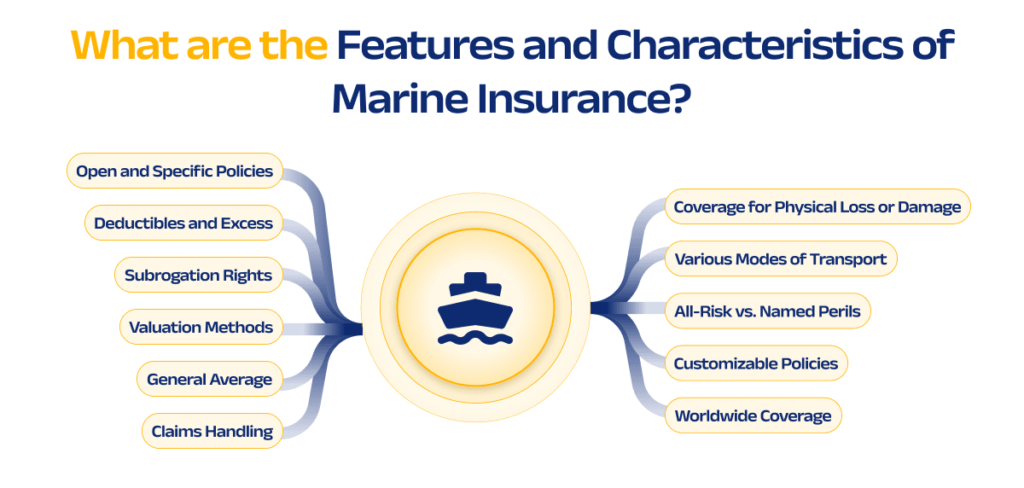

What are the Features and Characteristics of Marine Insurance?

1.Coverage for Physical Loss or Damage: Marine cargo insurance covers the loss or damage to goods and cargo during transportation. This can include damage from accidents, theft, fire, natural disasters, and other unforeseen events.

2. Various Modes of Transport: This insurance can apply to various modes of transportation, including shipping by sea, air, road, rail, or even a combination of these. It is adaptable to the specific needs of the cargo and the chosen method of transport.

3. Customizable Policies: Marine cargo insurance policies are highly customizable. Businesses can tailor their policies to suit their unique cargo, routes, and risk tolerance. Coverage can be adjusted to include or exclude specific risks or perils.

4. Worldwide Coverage: Marine cargo insurance provides coverage for shipments that travel across international borders and through different countries. It offers protection throughout the entire journey, from the moment the goods leave the seller’s premises until they reach the buyer’s destination.

5. All-Risk vs. Named Perils: Policies can be either “all-risk” or “named perils.” All-risk policies cover a broad range of perils unless specifically excluded, whereas named perils policies only cover specific risks explicitly listed in the policy.

6. Valuation Methods: Marine cargo insurance policies typically offer multiple valuation methods for determining the insured value of the cargo. Common methods include invoice value, market value, and cost-plus freight.

7. Open and Specific Policies: Open policies provide continuous coverage for an insured’s cargo shipments over a specified period, while specific policies cover a single shipment or a series of shipments between specific locations.

8. General Average: Marine cargo insurance often includes provisions for the general average. This means that if a ship experiences a major incident, such as jettisoning cargo to save the vessel, all parties involved (insured cargo owners and the shipowner) share the loss proportionately.

9. Subrogation Rights: In the event of a loss, the insurer may have the right to subrogate, which means they can seek reimbursement from third parties responsible for the loss. This helps to recover some or all of the insurance payout.

10. Deductibles and Excess: Policies may include deductibles (the portion of the loss that the insured must cover) and excess (the maximum amount the insurer will pay in the event of a loss), which can affect the cost of the insurance premium.

11. Claims Handling: Insurers typically have established procedures for filing claims in the event of a loss. Prompt and accurate reporting of losses is crucial to the claims process.

How does Marine Insurance Work?

In a marine insurance policy, the insurer assumes the responsibility for the goods, thus shifting the liability away from the parties and any related intermediaries. This policy insures the items against potential loss or damage and hence can be purchased by an exporter to safeguard the exported goods against loss or damage.

The transporter may be held liable if the products are damaged or lost while in transit, though usually compensation is given on a “per package” or “per consignment basis.” In this situation, the insurance coverage might not be enough to pay for the cost of the sent products. Therefore, exporters prefer to ship their goods once they have been protected by an insurance company.

To fulfil the requirements of an export contract, marine insurance is required. The exporter must obtain marine insurance to safeguard their bank or buyer interests and fulfill their contractual duties in order to comply with agreements like Cost Insurance And Freight (CIF) or Carriage And Insurance Paid (CIP). Delivered Duty Paid (DDP) and Delivered Duty Unpaid (DDU) terms do not need the seller to provide product insurance, but in practice, they typically do.

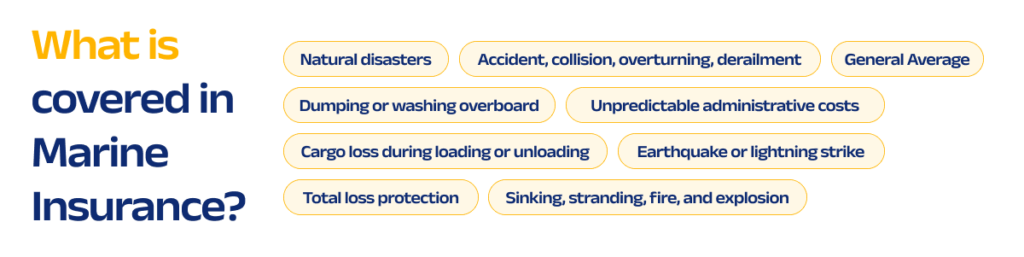

What is covered in Marine Insurance?

· Total loss protection

· Earthquake or lightning strike

· Sinking, stranding, fire, and explosion

· Dumping or washing overboard

· Natural disasters

· Unpredictable administrative costs

· Accident, collision, overturning, derailment

· Cargo loss during loading or unloading

· General Average

What all are not covered by Marine Insurance?

While the specific terms and conditions of marine insurance policies can vary, there are several common exclusions and limitations typically found in most marine insurance policies. These may include:

· Packing is inadequate or unsuitable.

· The insured committed a willful act.

· Normal weight loss or volume loss,

· Liquid leakage or normal wear and tear of the insured item.

· Delay of goods

· The subject matter insured has a vice or nature inherent in it.

· Unsuitability/unseaworthiness of the conveyance

· Owners, managers, or operators of the vessel/carrier defaulting on their financial obligations.

The footnote:

As we draw the final lines on this exploration, we have seen that marine insurance remains the steadfast anchor that enables businesses, traders, and adventurers to traverse uncertainties with confidence. It is through the collective efforts of insurers, underwriters, brokers, and stakeholders that the maritime world continues to prosper, knowing that even in the face of adversity, a lifeline exists.

In the maritime world, where the only constant is change, marine cargo insurance remains a beacon of stability. It is not just a story of risk mitigation but a testament to human resilience. Let us sail forward with the knowledge that in the heart of uncertainty, marine cargo insurance stands as an unwavering ally, guiding us toward new horizons and opportunities yet to be discovered.

Frequently Asked Questions (FAQs)

1. What is a constructive total loss in marine insurance?

A constructive total loss in the context of marine insurance refers to a situation in which the covered vessel or carrier has sustained damage to the point that the cost of repairing it exceeds its worth. Usually, a vessel or carrier is deemed to be in a constructive total loss when the cost of repairing it surpasses a predetermined percentage of its worth, which is often between 75% and 90%. Instead of covering the cost of the repairs in this scenario, the insurer will often pay the insured the full value of the vessel or carrier, less any deductible.

2. What is the general average in marine insurance?

A shipowner, at times, may intentionally sacrifice part of his cargo or vessel in order to avert a greater loss or damage to the ship or other cargo on board. In such situations, the general average principle becomes applicable in maritime law. This principle says that all parties having an interest in the vessel or the cargo, including the owners of the cargo and the vessel, are proportionately responsible for the loss or damage in such circumstances.

3. What is the Marine Insurance Act 1963?

On August 1st, 1963, the Marine Insurance Act, 1963 was first introduced in India with the intention of regulating the activities of marine insurance businesses for cargo, hull, and freight. The act describes the rights and obligations of all parties who participate in marine insurance transactions, including insurers, insureds, and brokers. This Act provides a framework for marine insurance contracts. It outlines the fundamental ideas of marine insurance, such as the necessity for an insurance contract to be founded on a legitimate insurable interest.

Read more about Single Transit Policy in Marine Insurance