It is an agreed fact that any business, no matter how well it is managed, can be just one unexpected event away from incurring serious financial loss. A fire at your warehouse, a customer lawsuit, or a data breach exposing sensitive records should not be considered remote possibilities alone. They are challenges that businesses across India face regularly, often unexpectedly. Without adequate protection, a single incident can drain years of hard-earned capital in weeks.

This is precisely where commercial insurance becomes a ‘must-have’ for you. It transfers your financial risk to an insurer, keeping your operations alive even when the worst happens.

By the end of this detailed guide, you will understand what commercial insurance is, the different types available, how coverage works, what it costs, and how to choose the right policy for your business.

Let’s proceed then!

Key Takeaways:

- Commercial insurance protects businesses from financial losses caused by property damage, lawsuits, cyber incidents, employee injuries, and disruptions.

- Different commercial insurance types address specific risks, including liability, property, cyber, marine, professional indemnity, and D&O coverage.

- Commercial insurance costs can vary depending on industry, business size, location, claims history, coverage limits, and specific risk exposure.

- Businesses can reduce premiums through risk management measures, policy bundling, higher deductibles, and maintaining a strong claims record.

- Choosing the right policy requires assessing business risks, comparing insurers, reviewing exclusions, and choosing appropriate coverage limits.

What Is Commercial Insurance?

Commercial insurance is a type of insurance that protects businesses from financial losses arising from property damage, lawsuits, employee risks, cyber incidents, and operational disruptions.

In simple terms, it is a contractual arrangement whereby a business pays a premium to an insurance company. In return, the insurer promises to cover certain specified losses up to an agreed limit. This arrangement transfers the financial risk from the business to the insurer. Thus, it enables companies to conduct their operations without the constant worry of an unexpected loss.

Every business, irrespective of its size, industry, or revenue, is exposed to a different set of risks. Commercial insurance in India is rapidly evolving as businesses realise that a well-crafted policy is not just a regulatory formality. Rather, it’s a genuine source of competitive and operational advantage.

How Commercial Insurance Works

The operations of a commercial insurance policy follow a very simple loop. The business identifies its risks and gets in touch with an insurer who recommends suitable coverage. The insurer assesses the risk profile and quotes an insurance premium. The business pays this amount monthly or annually to keep the policy active.

Once the policy is in force, the business is covered for the events specified in the agreement. If any unfortunate event happens to your business operations and it’s covered by your business insurance policy, you can submit a claim. The insurer conducts a claim audit, checks it against the policy terms, and issues a payout either to the business directly or to the third party, based on how the claim is handled.

Commercial Insurance vs Business Insurance: Are They Different?

This is one of the most common questions that business owners and finance managers ask. The short answer: they are largely the same thing, but the terminology matters in different contexts. Here is a clear comparison.

| Factor | Commercial Insurance | Business Insurance |

| Meaning | A formal term used in the insurance industry and legal documents | A colloquial term commonly used by small business owners |

| Usage | Preferred in corporate, regulatory, and broker communications | Used more in everyday business conversations |

| Coverage | Covers the complete spectrum of business risks including liability, property, employees, cyber, and others | Offers the same broad coverage. The term is interchangeable in most markets |

| Common Users | Large enterprises, SMEs, corporates, manufacturers & tech firms | Freelancers, small businesses, startups, & sole proprietors |

In practice, when you speak to a commercial insurance expert, they will use both commercial insurance and business insurance interchangeably. What matters most is understanding the specific policies bundled within any given plan. Do not go by only the label on the package.

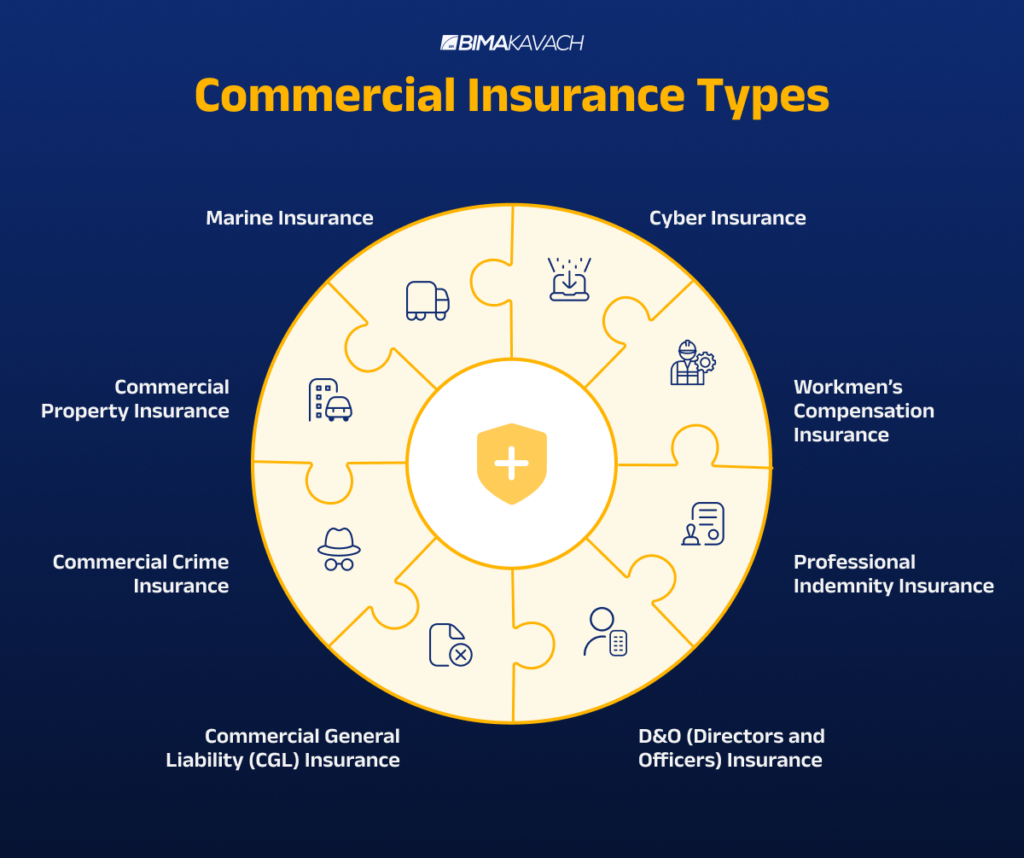

Types of Commercial Insurance: A Complete Breakdown

There is no single, one-size-fits-all solution when it comes to commercial insurance types. Different industries, business models, and operational profiles call for different coverage combinations. Here is a detailed look at the most critical types every business should know about.

| Insurance Type | Covers | Who Needs It |

| Commercial General Liability Insurance | Third-party bodily injury, property damage, legal costs | All businesses that interact with customers or the public |

| Commercial Property Insurance | Office, equipment, inventory, fixtures against damage or loss | Businesses with physical assets or premises |

| Workmen’s Compensation Insurance | Employee injuries, medical costs, lost wages | Any business with employees |

| Professional Indemnity Insurance | Errors, omissions, negligence in professional services | Consultants, lawyers, doctors, IT firms |

| Commercial Crime Insurance | Theft, fraud, embezzlement by employees or third parties | Retail, finance, warehousing businesses |

| Cyber Insurance | Data breaches, ransomware, cyber liability | Tech companies, e-commerce, any data-driven business |

| Marine Insurance | Goods in transit by sea, road, or air | Importers, exporters, logistics companies |

| Directors & Officers (D&O) Insurance | Personal liability of company directors and officers | Corporations, startups, publicly listed companies |

| Commercial Vehicle Insurance | Damage, theft, third-party liability for commercial vehicles | Fleet operators, logistics, delivery businesses |

Commercial General Liability Insurance

This is the basic insurance policy almost every business needs. Commercial General Liability (CGL) Insurance covers your business if a third party (a customer, vendor, or visitor) suffers bodily injury or property damage because of your operations. It also covers the legal defence costs associated with such claims, even if you are not at fault.

In India, just a single incident of a customer falling in a store or the customer claiming that your product has caused him/her harm can take you to court. Such legal battles can cost lakhs of rupees. In such instances, CGL acts as your financial shield.

Commercial Property Insurance

Commercial Property Insurance covers your business’s tangible assets, like the office building (if you are the owner ), furniture, equipment, stock, and fixtures, against covered risks such as fire, flood, burglary, and natural disasters. This insurance will help you recover and rebuild your business after major damage to your assets, without using your working capital.

If your business is located in a flood-prone area or in areas with high theft risk, this coverage can become a matter of survival. The insurance premium for property coverage depends on the declared value of assets and the location of the premises.

Workmen’s Compensation Insurance

The Employees’ Compensation Act, 1923, mandates that most Indian employers should compensate workers in case of injuries or diseases originating from their work. Workmen’s Compensation Insurance covers these legal obligations. These can include the cost of medical treatment, compensation for permanent disability and death benefits to the family of the deceased employee.

Besides fulfilling the legal requirements, this insurance also saves businesses from the financial distress caused by accidents at the workplace. In certain sectors like construction or manufacturing, such financial impact can be both frequent and severe.

Professional Indemnity Insurance

This business insurance policy is often purchased by consultants, doctors, lawyers, architects, IT firms, and financial advisors. A Professional Indemnity Insurance policy covers claims related to alleged professional negligence or errors in service delivery.

Commercial Crime Insurance

Internal fraud is one of the most overlooked threats to the fortunes of businesses. Commercial Crime Insurance, also known as fidelity insurance, protects against financial losses caused by employee theft, embezzlement, forgery, or fraud by third parties.

Cyber Insurance

Includes cover for first and third-party losses resulting from a cyber event. These losses may include data recovery costs, business interruption resulting from system downtime or delays, regulatory fines, and customer notification costs. Cyber Insurance has emerged as one of the fastest-growing business insurance types in India, thanks to the rise in digitisation.

Marine Insurance

Covers loss or damage to goods during transit, whether by sea, road, rail, or air. A Marine Insurance policy is critical for importers, exporters, and logistics companies operating across India or internationally.

Directors & Officers Insurance

Protects the personal assets of company directors and senior officers when they are personally sued for alleged wrongful acts in their management capacity. D&O Insurance provides essential corporate insurance coverage for any company with an independent board or external investors.

Commercial Vehicle Insurance

Commercial vehicle insurance is intended for vehicles that a business uses for its activities – from delivery vans and taxis to goods carriers and other means of worker transportation. This is a mandatory insurance class in India under the Motor Vehicles Act for any vehicle used commercially. It covers third-party liability, own damage, and, in comprehensive plans, personal accident cover for the driver.

What Is Commercial Umbrella Insurance?

Imagine your Commercial General Liability policy has a limit of ₹1 crore. A lawsuit hits your business, and the damages awarded by the court are ₹3 crore. Your primary policy pays out ₹1 crore and then stops. The remaining ₹2 crore? Without a commercial umbrella policy, which comes directly from your business assets.

Commercial umbrella insurance is a supplementary policy that activates once the limits of your primary commercial insurance coverage are exhausted. It provides an extra layer of financial protection over and above your existing policies. Thus, it acts as a safety net above your safety net.

It is worth noting that umbrella insurance does not replace your primary policies. This coverage will be triggered only after the underlying limits are fully consumed. That’s why it is a highly cost-effective way to increase your total coverage without having to buy separate high-limit policies for individual risk categories.

What Does Commercial Insurance Cover?

Knowing exactly what commercial insurance will cover is a must if you want to make sure your business is neither over-insured (wasting on premiums) nor under-insured (exposed to uncovered losses). Below, you will find a detailed description of the typical ins and outs of commercial insurance coverage.

What Is Covered

- Physical property damage to owned or leased premises, equipment, and stock

- Third-party liability for bodily injury or property damage caused by your business operations

- Legal expenses, including attorney fees, court costs, and settlement amounts

- Employee injuries, occupational illnesses, and death benefits under workers’ compensation

- Cyber losses, including data breach costs, ransomware response, and regulatory fines

- Revenue loss or business interruption when operations are halted due to a covered event

- Professional errors and omissions resulting in client financial loss

- Crime losses, including employee theft, forgery, and third-party fraud

What Is Not Covered

- Employee injuries that fall outside the scope of the workers’ compensation schedule

- Intentional acts or deliberate damage caused by the business owner or employees

- General wear and tear, gradual deterioration, or lack of maintenance

- Certain natural disasters that are specifically excluded (some flood and earthquake events)

- Fraud or misrepresentation by the insured when taking out the policy

- Pre-existing damage or losses that occurred before the policy inception date

Commercial Insurance Cost : How Much Does It Cost?

A common question most business owners often ask is how much insurance coverage they need to purchase. Well, there is no single figure we can put our fingers on. This is because premiums are determined by considering multiple factors discussed below. By familiarising yourself with these main price determinants, you can plan your finances efficiently.

Factors Affecting Commercial Insurance Cost

- Nature and type of business: High-risk industries such as manufacturing, construction, and food processing will see increased premiums compared to low-risk sectors such as consultancy or software development.

- Business size and revenue: Bigger businesses with more employees, assets, and turnover will pose greater risk exposure to insurers. As a result, premiums tend to be on the higher side.

- Location: Businesses in locations prone to floods, theft, or civil unrest will need to pay more for property and liability coverage.

- Claims history: A business with a track record of frequent claims is normally kept in a risky category by insurers and needs to pay higher commercial insurance premiums.

- Coverage limits and deductibles: The more coverage you want, the more you have to pay. Also, the higher the deductible(the amount you pay before an insurance claim gets processed), the lower the premium.

- Number of employees: This number directly influences workers’ compensation costs and general liability exposure.

- Industry-specific risks: Businesses that handle dangerous substances, operate heavy machinery, or have access to confidential client data are bound to face specialised risk surcharges.

Average Commercial Insurance Cost Examples

The following figures are indicative estimates based on industry benchmarks for commercial insurance in India. Actual premiums will vary based on insurer, risk assessment, and negotiated terms.

| Business Type | Approx. Annual Premium Range | Common Policies Included |

| Small retail shop | ₹15,000 – ₹40,000 | Property, CGL & Crime |

| IT / Software startup (10–50 employees) | ₹50,000 – ₹2,00,000 | Professional Indemnity, Cyber & Workmen’s Compensation |

| Manufacturing unit (mid-size) | ₹1,50,000 – ₹5,00,000 | Property, Workmen’s Compensation, CGL & Marine |

| Restaurant / Hospitality business | ₹40,000 – ₹1,20,000 | Property, CGL & Workmen’s Compensation |

| E-commerce / D2C brand | ₹60,000 – ₹2,50,000 | Cyber, Product Liability, Marine & Property |

| Construction company | ₹2,00,000 – ₹10,00,000+ | CGL, Property, Umbrella & Workmen’s Compensation |

Which Businesses Need Commercial Insurance?

The simple answer is this: nearly every business needs commercial insurance in some form. That said, different policies will be suitable for different businesses according to factors like the nature of the business, the level of risk involved, and the regulatory requirements. Here is a breakdown of these businesses.

Small Businesses

One common mistake small business owners make is thinking they are too small to be sued or to experience significant losses. This can be a fatal misconception. A single customer injury claim or a fire destroying your inventory can easily wipe out a small business with limited reserves. A basic commercial insurance policy, including CGL and property coverage, would be a wise step for any small business.

Manufacturers

Manufacturing involves heavy equipment, raw materials, large teams, and complicated supply chains, each of which entails risk. It is almost impossible for a manufacturing entity in India to operate these days without Property Insurance, Workmen’s Compensation Insurance, Product Liability Insurance, and Marine Insurance.

Startups

A lot of startup founders tend to push insurance down the list of priorities and thus prioritise growth over protection. But investors, clients, and enterprise customers often ask for proof of adequate coverage before entering into contracts. Professional indemnity, D&O, and cyber insurance are certain critical insurance types for tech startups that deal with data or provide digital services.

Tech Companies

Technology companies face a very specific set of risks, like IP infringement claims, cyber breaches, software errors leading to client losses, and non-compliance with data privacy requirements. Cyber Insurance and Professional Indemnity Insurance are two main insurances that any tech company should have.

Professional Services

Occupations like lawyers, chartered accountants, architects, doctors, and management consultants have a high risk of professional liability. A situation where your client holds you responsible for the wrong advice can easily result in a costly lawsuit. If you are someone whose livelihood depends on delivering expert advice or services, Professional Indemnity Insurance is quite essential for you.

Businesses With Employees

The moment you bring in your first employee, your risk level is going to change quite a bit. Workers’ Compensation Insurance becomes mandatory for most employers under Indian law. Besides, Employment Practices Liability and Group Health Insurance might be options to consider as they could protect your employees and business against HR related claims.

How to Choose the Right Commercial Insurance Policy

Selecting the right commercial insurance policy is all about identifying the coverage that suits your unique risk profile and business goals. A good way to approach this is by breaking down the task into definite steps.

- Identify risks: Begin with a formal risk assessment. What are the top perils that could hit your business the hardest? Loss of property, breach of cybersecurity, product recall, or legal disputes? The answer will vary significantly, depending on the type of your industry and business. Be honest and comprehensive.

- Assess liabilities: Understand your legal obligations (e.g., mandatory workmen’s compensation), contractual requirements from clients, and any industry-specific regulatory mandates.

- Determine coverage limits: Decide how much financial exposure your business can absorb independently and set your coverage limits to protect against losses beyond that threshold.

- Compare policies: The coverage terms for commercial insurance policies vary significantly from one insurance provider to another. Two policies with identical premium quotes can have a wide variation in coverage offered, claim settlement ratios, and exclusion clauses.

- Review exclusions: This is perhaps the most important aspect that businesses fail to consider well enough. Exclusions are the things that your insurer will not cover. Misunderstanding or ignoring exclusions is one of the biggest causes of claim rejections in business insurance policies.

Common Mistakes Businesses Make While Buying Commercial Insurance

Even experienced business owners make costly errors when purchasing coverage. Here are the most common pitfalls and how to avoid them.

- Underinsuring assets: Let’s put it straight! Underinsuring to reduce insurance premiums is a mistake. When a large claim arises, inadequate business insurance coverage will mean you will be personally liable for the residual loss. Always make sure your insurance coverage aligns with the realistic replacement or compensation values of your assets and liabilities.

- Ignoring policy exclusions: Flipping through a commercial insurance policy document and missing the fine print of exclusion clauses has left many businesses stranded when it counts. Always read the full policy wording and not just the summary brochure.

- Choosing the cheapest plan: A low commercial insurance premium often signals limited coverage, high deductibles, or a weak claim settlement ratio. Prioritise value over cost. The cheapest policy is rarely the best policy.

- Buying wrong/insufficient coverage limits: Underestimating the scale of potential losses and choosing low limits is a common mistake, especially for liability and property coverage. In today’s litigious environment, damages can far exceed what business owners anticipate.

How to File a Commercial Insurance Claim

By doing everything right in filing a claim, a policyholder can almost ensure a smooth payout. Here is a step-by-step guide for filing a commercial insurance claim.

- Inform your insurer immediately: Most insurance contracts specify a limited period during which you must notify the insurer. Inform your insurer/broker immediately after the covered event occurs. A delay here may result in claim rejection.

- Document the loss properly: Capture a picture or make a video of the damage, get a written statement from witnesses, gather bills and receipts for damaged items, and secure any physical evidence.

- File an FIR, if required: For losses related to theft, burglary, or crime, an FIR from the local police is required for the claims processing.

- Submit the claim form & supporting documents: Fill out the insurer’s claim form properly and enclose all supporting documents. These may consist of the policy copy, FIR (if any), photographs, invoices, medical reports (for WC Insurance), and any third-party communications.

- Cooperate with the loss assessor: Most often, the insurer will designate a loss assessor or surveyor to investigate the claim. Fully extend assistance, grant access to the premises, supply the requested records, and respond to queries promptly.

- Review the settlement offer: After the insurer issues a settlement, evaluate it carefully against your specific policy terms. If you feel the settlement is unfair, you have the right to dispute it. Engage your broker or a public adjuster for help.

Why Commercial Insurance Is Important for Businesses

On top of providing financial protection, it can be a strategic tool for ensuring the long-term viability and success of your business. Here are the reasons why-

- Business continuity: After a disaster strikes, it gives your business the financial resources to recover and function again without using up working capital or falling into the vicious cycle of debt.

- Legal & regulatory compliance: A lot of commercial insurance policies are legally mandated in India. These may include Workmen’s Compensation, Third-party Vehicle Insurance, and public liability coverage ( in some sectors). The failure to comply can lead to fines, penalties, and legal liability.

- Trust: Big clients, Government contracts, and institutional investors usually require companies to present evidence of adequate insurance coverage before entering into agreements. Being insured is considered a symbol of your professionalism, stability, and willingness to take responsibility.

- Financial protection to stakeholders: Just like the employees who depend on workmen’s compensation, the shareholders who expect smooth business operations are also protected by commercial insurance.

Frequently Asked Questions

Is commercial insurance mandatory for businesses in India?

Certain types of commercial insurance are legally mandatory in India for specific situations. For example, most employers must get Workmen’s Compensation Insurance as per the Employees’ Compensation Act. The Motor Vehicles Act makes third-party motor insurance mandatory for all commercial vehicles. Also, Public Liability Insurance is a statutory requirement for certain industries such as factories and public utilities. While it is not mandatory for all businesses, specific types of policies are compulsory depending on your business type and sector.

What is the difference between commercial insurance and liability insurance?

Commercial insurance is an umbrella term covering various types of risks, like property, liability, employees, cyber, crime, and professional errors. However, Liability insurance is just a subset of commercial insurance that addresses your legal responsibility to third parties. It covers compensation and legal expenses related to injury, property damage, or professional negligence. Simply put, all liability insurance is a form of commercial insurance, but not all commercial insurance is liability insurance.

How much commercial insurance coverage does a business need?

The amount of coverage depends largely on factors like industry, business size, the value of assets, the number of employees, and the nature of your client contracts. For example, a small services company might purchase a ₹50 lakh liability coverage. On the other hand, a big manufacturing plant might need ₹5 crore or more across several policies.

What is commercial umbrella insurance used for?

Commercial umbrella insurance offers an extra buffer of financial security that goes beyond your standard commercial insurance coverage. It comes into play when a covered claim goes beyond the limit of the underlying policy. In such instances, it covers the excess up to the umbrella policy’s limit. Generally, this insurance is used by businesses that operate in risky areas, have large public footfall, and companies that regularly enter into high-value contracts that require significant liability coverage.

Can small businesses buy commercial insurance in India?

Yes, they can. Commercial insurance in India is accessible to businesses of all sizes. Besides, many insurers have special offerings for small and medium enterprises (SMEs). For instance, the Micro, Small and Medium Enterprise (MSME) insurance packages combine essential coverage (property, liability, and workmen’s compensation) at reasonable prices. Small businesses should consult a commercial insurance company that can figure out the perfect coverage mix for them, without overspending on unnecessary policies.