When it comes to protecting our homes and properties from unforeseen disasters, Fire Insurance plays a crucial role. Among the many terms and acronyms associated with Fire Insurance Policies, one that often catches the attention is STFI. The concept of STFI within a Fire Insurance Policy is designed to offer additional protection and flexibility to policyholders. It ensures that their belongings remain safeguarded during the temporary relocation period, thus providing peace of mind amidst the chaos that follows a fire incident.

In this article, we will delve deeper into the meaning of STFI in a Fire Insurance Policy. We will explore the scope of coverage it provides, the conditions under which it applies, and the significance of this provision for policyholders. This informative journey will empower you to make well-informed decisions and ensure the protection of your property, even in the face of unexpected events.

Let’s start with the basics first!

The Meaning of STFI in a Fire Insurance Policy

STFI stands for “Storm, Tempest, Flood, and Inundation.” STFI cover is an add-on cover purchased along with a Standard Fire & Special Perils Insurance Policy which protects one’s property against loss caused by any of the covered perils. The Fire Insurance Policy Wordings for STFI Cover typically reads as “Loss or Damage caused by Storm, Tempest, Cyclone, Typhoon, Tornado, Hurricane, Flood or Inundation excluding those originating from Volcanic Eruption, Earthquake or other convulsions of nature.”

In the event of a fire or any other covered peril, policyholders with this cover can find solace in the fact that their insurance policy provides coverage not only for the property situated at the insured premises but also for its temporary removal. This temporary removal can be due to a variety of reasons, such as repairs, renovations, or other circumstances that require the property to be relocated temporarily.

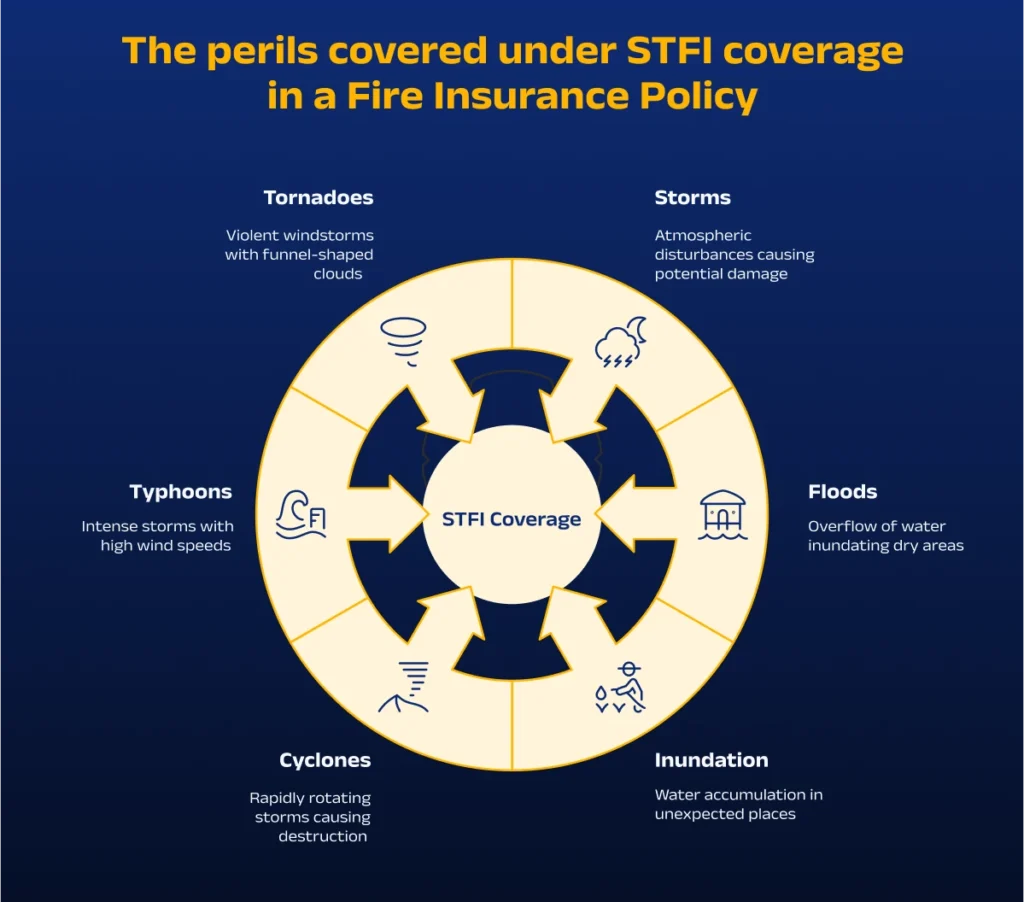

The Perils Covered Under STFI Coverage in a Fire Insurance Policy

The following are the precise definitions of the terms included under STFI coverage in a Fire Insurance Policy:

Storm and Tempest

In a Fire Insurance Policy, the phrases Storm and Tempest are typically used interchangeably. A storm is any type of atmospheric disturbance that can cause severe winds, lightning, rain, or hail. Storm is defined by the Oxford Dictionary as “very bad weather with strong winds and rain, and frequently thunder and lightning.” Also, a tempest is defined as “a violent windy storm usually accompanied by hail, rain or snow.”

Even though they are protected by the STFI Cover, the Storm Peril is distinct from the Flood Peril. Storms can create floods, however, flood is not the same as Storm and Tempest Peril. Storms are relatively common and normally do not cause significant damage to the insured’s property.

Floods

Flooding is the temporary inundation of normally dry terrain by water caused by the overflow of seas, lakes, dams, rivers, and so on, or by severe rainfall or groundwater bursting up. Thus, flood typically refers to water escaping its customary boundaries or accumulating rainfall in a certain area. Please note that flooding is not the same as water damage. Water damage typically occurs within houses, offices, and other structures and is caused by a burst or flow within the property. The primary distinction between a flood claim and a water claim is the source of the water.

In a flood, the water usually comes from a natural external source such as a river, sea, or dam, and two or more properties are damaged. However, in a water damage claim, the damage comes from inside the insured premises such as a home, office, etc., but the neighboring properties are not damaged.

Floods are common in many Indian states, hence flood insurance is an important component within the STFI cover of a Fire Insurance Policy.

Inundation

Inundation occurs when water accumulates in a normally dry location, causing water levels to rise. It is caused when a body of water overflows, drowning or submerging a dry area. As a result, the losses caused by inundation may be covered by the Fire Insurance Policy.

Cyclone

Cyclones are formed by atmospheric disturbances in the vicinity of a low-pressure area, and they are distinguished by rapid and destructive air circulation. Cyclones are frequently accompanied by intense storms and inclement weather. A cyclone can wreak havoc on a town or city, destroying numerous livelihoods and company sites. If it occurs, it has the potential to cause immense devastation and destruction. As a result, it is sometimes referred to as a violent storm. Cyclone Coverage is a critical component of STFI Coverage in a Fire Insurance Policy.

Typhoons and Hurricanes

Typhoons and hurricanes are two names for similar phenomena. A typhoon is a tropical storm, and the wind speed during a typhoon can reach 119 km/h. As a result, it may result in enormous destruction of insured property covered by the Fire Insurance Policy.

Hurricanes usually form over hot or warm waters, which can destroy insured property. As a result, hurricane-related losses are covered by the Fire Insurance Policy.

Tornado

Tornadoes usually happen on land, but tropical cyclones, typhoons, and hurricanes typically occur on water. On land, tornadoes typically generate vortices. As a result, if it occurs and the insured property is caught in the vortex’s transmission, there is no way for the property to get away from its involvement. As a result, the losses are caused by Tornado coverage under the Fire Insurance Policy.

Who Needs STFI Coverage in Fire Insurance?

Business owners who own or operate commercial properties, offices, factories, or warehouses may need STFI coverage as part of their Fire Insurance. This coverage protects their assets and operations against the potential damages caused by storms, tempests, floods, or inundation. So, any business which needs protection from natural calamities should take STFI cover as part of their standard SFSP Policy.

Developers and builders involved in construction projects may also require STFI coverage to protect their properties under construction. It safeguards against potential damages caused by storms, tempests, floods, or inundation during the construction phase. For the same reason, public institutions such as schools, hospitals, government offices, and non-profit organizations may opt for STFI coverage in their Fire Insurance Policies as well.

Conclusion:

From the discussion above, we have seen that STFI serves as a pivotal clause that ensures the insured property is adequately protected against fire-related risks. It guarantees that the policyholder will receive compensation for damages caused by fire, allowing them to rebuild and recover from such unfortunate incidents. Furthermore, STFI emphasizes the significance of fire prevention and safety measures, encouraging policyholders to take proactive steps in minimizing fire hazards and implementing effective fire prevention strategies.

Being informed about the presence and implications of STFI would empower you to make informed decisions when selecting Fire Insurance Policies, ensuring you have the right coverage in place. However, Fire Insurance is just one of several essential commercial insurance covers available in India. Having the right mix of these will help you map out a complete protection strategy for your operations.

For more information on any topics related to business and insurance, you may contact BimaKavach. Here, you can also get the best recommendation for any insurance product in just 5 minutes.